Cybersecurity in Fintech: Protecting Financial Data

In the fast-paced world of finance and technology, the emergence of Fintech (Financial Technology) has revolutionized the way we handle our money and conduct financial transactions. Fintech companies leverage cutting-edge technology to offer a wide range of financial services, from online banking and mobile payments to peer-to-peer lending and robo-advisors. While these innovations have undoubtedly made our lives more convenient, they have also given rise to new challenges, especially when it comes to the security of financial data.

In this comprehensive guide, we will delve into the importance of cybersecurity in fintech and explore the critical strategies, tools, and best practices that can help protect sensitive financial data from the ever-evolving threats in the digital landscape.

The Fintech Revolution and Market Highlight

The fintech industry has transformed the way we manage our finances. From mobile banking apps to digital wallets and peer-to-peer lending platforms, fintech has brought financial services closer to our fingertips. The fintech revolution has made banking more convenient, cost-effective, and accessible to a broader range of people, leading to significant advancements in the finance market.

The Importance of Cybersecurity in Fintech

However, with great convenience comes great responsibility. As fintech companies handle vast amounts of sensitive financial data, they have become prime targets for cybercriminals. These criminals are constantly devising new techniques to breach security measures and gain unauthorized access to valuable data, such as bank account details, personal identification information (PII), and credit card numbers.

The consequences of a successful cyberattack on a fintech company can be devastating. It can lead to financial losses, reputation damage, legal liabilities, and, most importantly, the compromise of customers’ financial security. Therefore, cybersecurity in fintech is not merely an option; it’s a critical necessity. This guide will explore the various aspects of cybersecurity in the fintech industry and provide insights into how companies can protect financial data and maintain the trust of their customers.

Understanding the Fintech Ecosystem

Before delving into cybersecurity measures, it’s essential to understand the Fintech ecosystem and the types of companies that operate within it. Fintech companies can be categorized into several key areas, each with its unique focus and challenges.

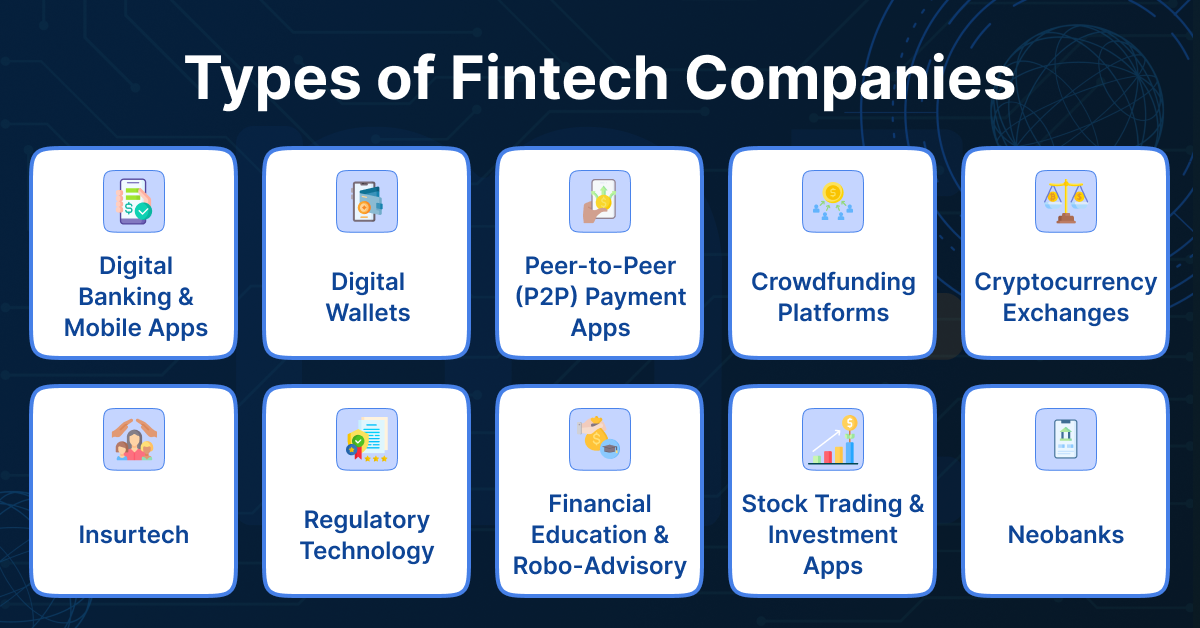

The Fintech Ecosystem: Exploring Different Fintech Players

Digital Banking and Mobile Apps:

Digital banks and mobile banking apps offer a complete range of banking services, from opening accounts to making payments, transferring funds, and managing investments, all through user-friendly mobile or web interfaces.

Peer-to-Peer (P2P) Payment Apps:

These apps enable individuals to send money to friends and family quickly and securely.

Digital Wallets:

Digital wallets store payment information and facilitate online and in-store purchases.

Crowdfunding Platforms

These platforms connect businesses, startups, or individuals seeking funding with a diverse group of investors or backers. Types include equity crowdfunding and peer-to-peer lending.

Cryptocurrency Exchanges

Platforms for buying, selling, and trading cryptocurrencies like Bitcoin and Ethereum.

Insurtech

Digital solutions in the insurance industry, known as insurtech, include fintech mobile apps and platforms that offer digital insurance policies, claims processing, and risk assessment using data analytics and AI. It won’t be wrong to state that the insurance industry is reshaping in a better way, thanks to the growing digital landscape!

Regtech (Regulatory Technology)

Regtech solutions help financial institutions comply with regulatory requirements more efficiently. This includes tools for regulatory reporting, monitoring, and risk management.

Peer-to-Peer Lending (P2P)

P2P lending platforms connect borrowers with individual or institutional lenders, eliminating the need for traditional banks.

Neobanks

Neobanks are fully digital banks that operate without physical branches. They provide a wide range of banking services online or through mobile apps, often with lower fees and more convenience.

Stock Trading and Investment Apps

Mobile apps like Robinhood and E-TRADE allow users to buy and sell stocks, ETFs, and other securities with low or no commissions.

Financial Education and Robo-Advisory Content

Platforms that provide educational content and personalized financial advice to help users make informed investment decisions.

The Growing Threat of Cyber Attacks in Fintech

Phishing Attacks:

Cybercriminals impersonate legitimate entities, often via email or websites, to trick users into revealing sensitive information, such as login credentials or credit card numbers.

Distributed Denial of Service (DDoS) Attacks:

Attackers flood fintech systems with traffic, rendering them inaccessible to legitimate users.

Malware and Ransomware:

Malicious software can infect systems and encrypt data, demanding a ransom for its release.

Insider Threats:

Employees or individuals with insider access may misuse their privileges to steal data or compromise security intentionally or unintentionally.

Third-Party Risks:

Fintech companies often rely on third-party service providers. If these providers have weak security, they can become entry points for attackers.

In the next sections of this guide, we will explore the importance of cybersecurity in fintech and the critical measures that fintech companies can implement to mitigate these threats and protect financial data effectively.

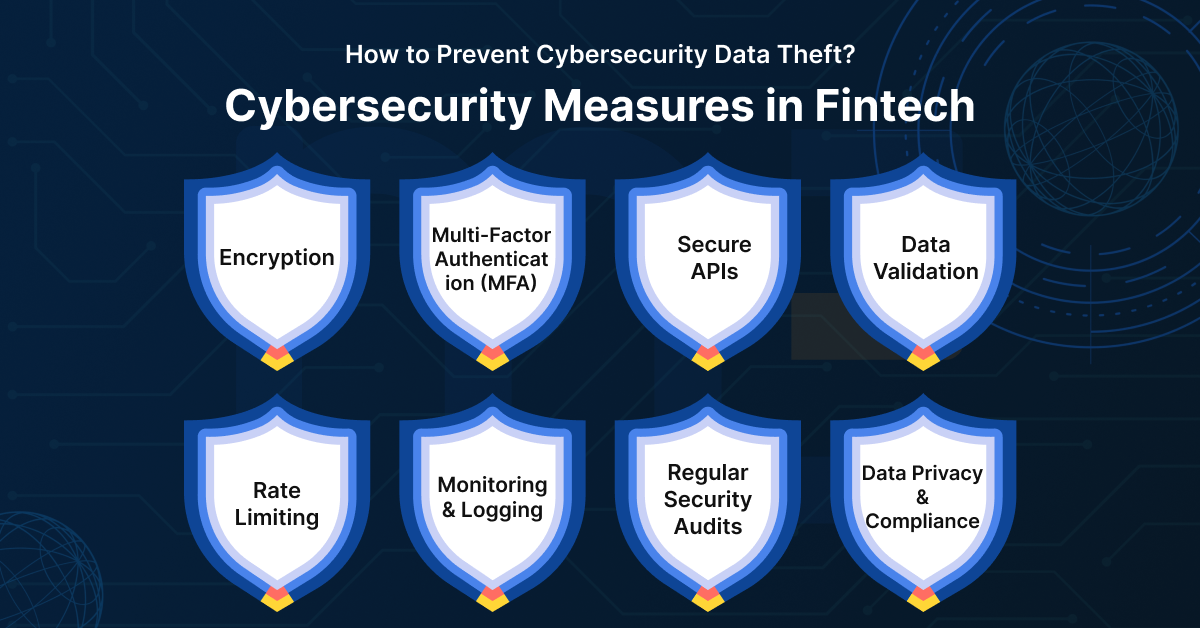

How to prevent Cybersecurity data theft? Cybersecurity Measures in Fintech!

Protecting financial data in the fintech industry requires a multi-layered approach to cybersecurity. Here are some essential measures that fintech companies should consider:

Encryption

Encryption is a fundamental component of data security. It involves converting data into a coded form that can only be read by someone with the decryption key. In the fintech industry, encryption is used to ensure that data is encrypted from the sender to the recipient, even within the fintech platform itself. Implementing strong encryption protocols and regularly updating them is crucial to maintaining data security.

Multi-Factor Authentication (MFA)

Multi-factor authentication adds an extra layer of security by requiring users to provide two or more forms of identification before granting access. Common factors include something the user knows (password), something the user has (smartphone or security token), and something the user is (biometric data like fingerprints or facial recognition). MFA significantly reduces the risk of unauthorized access, even if a password is compromised.

Secure APIs

Fintech companies often rely on Application Programming Interfaces (APIs) to connect with external systems and services. Ensuring that these APIs are secure is essential. Best practices for API security include Authentication and Authorization: Ensuring that only authorized parties can access the API and perform specific actions.

Data Validation

Validating data inputs to prevent attacks like SQL injection.

Rate Limiting

Implementing rate limiting to prevent abuse and DDoS attacks through API endpoints.

Monitoring and Logging

Continuously monitoring API activity and logging events for security analysis and incident response.

Regular Security Audits

Regular security audits and penetration testing can help fintech companies identify vulnerabilities in their systems. These audits should be conducted by third-party security experts to provide an unbiased assessment of security measures. Additionally, security audits should include testing incident response plans to ensure that the company is prepared to respond effectively to cyber threats. In the next sections, we will explore data privacy and compliance, as well as the importance of building a cybersecurity culture within fintech organizations.

Data Privacy and Compliance in Fintech Development

Data privacy and compliance are critical considerations for fintech companies. Regulatory bodies around the world impose strict requirements on the handling of financial data to protect consumers. One of the most well-known regulations is the General Data Protection Regulation (GDPR) in the European Union. However, various countries and regions have their own data protection laws.

GDPR and Other Data Protection Regulations GDPR, enacted in 2018, imposes stringent rules on the processing of personal data, including financial information. Key provisions include:

Data Consent

Companies must obtain clear and unambiguous consent to collect and process personal data.

Data Portability

Consumers have the right to request their data and transfer it to another service provider.

Data Breach Notification

Companies must report data breaches to the relevant authorities and affected individuals within 72 hours of discovery.

Data Protection Officers (DPOs)

Organizations handling large amounts of sensitive data may be required to appoint a DPO to oversee data protection efforts.

Fintech companies must not only comply with GDPR but also be aware of and adhere to data protection laws in their operating regions. In the next section, we will explore emerging technologies and the associated cybersecurity risks in fintech.

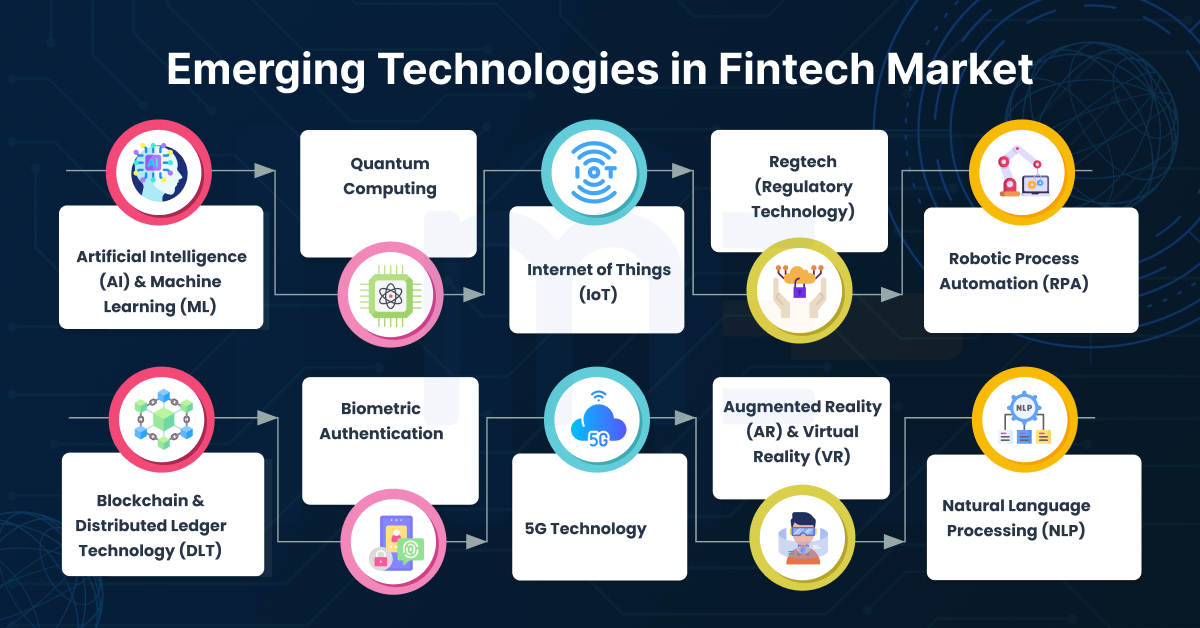

Emerging Technologies in Fintech Market:

The fintech industry is constantly evolving, driven by emerging technologies that have the potential to transform financial services and improve customer experiences. Here are some of the most prominent emerging technologies in fintech:

Artificial Intelligence (AI) and Machine Learning (ML)

Chatbots and Virtual Assistants:

AI-powered chatbots and virtual assistants provide customer support, answer queries, and assist with tasks such as account management and transaction tracking.

Predictive Analytics:

ML algorithms analyze vast amounts of data to make predictions about customer behavior, market trends, and investment opportunities.

Credit Scoring:

AI-driven credit scoring models use alternative data sources and behavioural analysis to assess creditworthiness more accurately.

Fraud Detection:

AI identifies unusual patterns and detects fraudulent transactions in real time, enhancing security.

Blockchain and Distributed Ledger Technology (DLT):

Cryptocurrencies:

Blockchain underlies cryptocurrencies like Bitcoin and Ethereum, enabling secure and transparent transactions.

Smart Contracts:

Self-executing smart contracts automate contract execution and enforcement, reducing the need for intermediaries.

Cross-Border Payments:

Blockchain can streamline cross-border payments, reducing costs and settlement times.

Quantum Computing:

Security:

Quantum computers have the potential to break current encryption methods, prompting the development of quantum-resistant encryption algorithms.

Portfolio Optimization:

Quantum computing can analyze complex financial models and optimize investment portfolios.

Biometric Authentication:

Fingerprint Recognition:

Biometric authentication methods like fingerprint recognition and facial recognition enhance security for mobile banking and online transactions.

Voice Recognition:

Voice biometrics can be used for authentication and fraud prevention.

Internet of Things (IoT):

Connected Devices:

IoT devices can monitor and transmit financial data, such as vehicle telematics for auto insurance pricing or wearable devices for health insurance tracking.

Smart Payments:

IoT-enabled devices like smart fridges can initiate automatic grocery reordering and payments.

Regtech (Regulatory Technology)

Compliance Automation:

Regtech solutions use AI and data analytics to automate regulatory compliance, monitor transactions, and ensure adherence to financial regulations.

KYC/AML (Know Your Customer/Anti-Money Laundering):

Regtech tools streamline identity verification and customer due diligence processes.

5G Technology

High-Speed Connectivity:

5G networks enable faster and more reliable mobile banking and payment transactions.

IoT Connectivity:

5G facilitates the connection of a larger number of IoT devices, enhancing the scope of financial services.

Decentralized Finance (DeFi)

DeFi Platforms:

DeFi projects leverage blockchain technology to create decentralized lending, borrowing, and trading platforms, bypassing traditional intermediaries.

Stablecoins:

Stablecoins, often built on blockchain, offer price stability and are used in DeFi applications.

Open Banking:

API Integration:

Open banking initiatives enable financial institutions to share customer data securely through APIs, leading to enhanced financial services and improved competition.

Edge Computing

Real-Time Data Processing:

Edge computing brings data processing closer to the source, allowing for real-time analytics in financial applications, such as fraud detection.

Robotic Process Automation (RPA):

Automated Back-Office Operations:

RPA bots can perform repetitive banking and financial operations tasks, reducing errors and improving efficiency.

Digital Identity Solutions:

Self-Sovereign Identity (SSI):

SSI enables individuals to securely control and share their digital identity, enhancing privacy and security in financial transactions.

Tokenization

Asset Tokenization:

Tokenization of assets like real estate and fine art enables fractional ownership and more accessible investment opportunities.

Augmented Reality (AR) and Virtual Reality (VR):

Immersive Banking Experiences:

AR and VR can create immersive customer experiences for virtual branch visits and financial data visualization.

Natural Language Processing (NLP):

Sentiment Analysis:

NLP can analyze news and social media sentiment to inform trading decisions and investment strategies.

These emerging technologies are driving innovation and disruption in the fintech sector, enabling financial institutions and startups to offer more sophisticated, efficient, and customer-centric solutions. As these technologies continue to mature, they will likely play an increasingly central role in the future of finance.

Top B2B Fintech Companies and How Digital Innovation Made Them Successful

Revolut

Revolut identified the need for the use of digital technology and mobile apps to make banking easier for users more than a decade ago. In the early 2010s, the founders of Revolut saw that smartphone adoption and use were on the rise and that there was a market for digital banking apps. They started working on a digital banking app and launched it in 2015. Its primary appeal was the ease of sending and receiving money, cryptocurrency, and P2P payments all over the world. It offered all transactions at interbank exchange rates and charged no fees on currency exchanges.

The app quickly gained popularity because it was easy to use and was a faster and more secure alternative to conventional banking. The app and its services are a good example of using digital innovation to win over a largely untapped market.

Wise

Wise took an age-old, tried-and-tested business model and modernized it. The founders realized that banks charge a hidden fee by offering less favourable exchange rates. They created an MVP using the Grails framework, with one of the founders writing the first few thousand lines of code himself. They spread the word through unpaid marketing campaigns to get their first few users.

The company started with a peer-to-peer model and cut out bank exchange fees entirely by matching people who wanted to transfer money from one country to another with others who wanted to do the opposite. When a match was not available, Wise used its own funds.

Paddle

Paddle was founded in 2012 to help SaaS companies in subscription management, renewals, and reporting. The company also built regulation compliance, fraud detection, and payment routing into its platform, giving SaaS companies all the features they need for payment management and transaction monitoring.

Offering a complete payment infrastructure, it takes away the need for SaaS companies to maintain a security tech stack just for payment management. For example, a SaaS company that uses Paddle doesn’t need a fraud detection system, compliance software, and invoicing software, among others. Instead of dedicating resources to managing and integrating a vast technology stack, these companies can simply use Paddle to handle payments and focus on their core products.

Thought Machine

Thought Machine identified the need for legacy banks to modernize their digital infrastructure back in the early 2010s and created a banking platform called Vault to do just that.

Through Vault, Thought Machine gives legacy banks everything they need to move from legacy banking systems to a modern, cloud-native core banking platform. The platform enables banks and financial institutions to provide their customers with secure and personalized banking services while also streamlining their internal operations.

Conclusion

The fintech industry has redefined how we manage our finances, but with this convenience comes the responsibility of safeguarding sensitive financial data. Cybersecurity in fintech is not a one-time effort but an ongoing commitment to protecting customer trust and complying with data protection regulations.

Fintech companies must implement robust security measures to protect financial data, including encryption, multi-factor authentication, and secure APIs. They must also prioritize data privacy and compliance with regulations like GDPR. Building a cybersecurity culture within the organization and effective employee training and incident response plans are crucial in mitigating threats. Fintech companies should also stay vigilant against emerging technologies and their associated risks.

Level up your knowledge with expert insights and resources straight to your inbox

As the fintech landscape continues to evolve, maintaining the security and trust of customers will remain a top priority. By following the best practices outlined in this guide, fintech companies can navigate the cybersecurity challenges of the digital age and ensure the safety of financial data for years to come.

Do you like this article? Let's share!

Shoeb Zahoori

Shoeb Zahoori is a Technology Advisor and Digital Transformation Contributor with a focus on sales growth across multiple service offerings and geographies. He enjoys talking about technology solutions, artificial intelligence, automation, IoT and blockchain.